Reprinted with Permission Intro deck A feasibility study is not just a report. It is often the document that stands between a project and a loan approval, credit decision, investment committee vote, board…

Reprinted with Permission Intro deck A feasibility study is not just a report. It is often the document that stands between a project and a loan approval, credit decision, investment committee vote, board resolution, or public-sector green light. That is why buyers should not begin by asking which firm is most famous.

The better question is which provider is best suited to the assignment, the audience that will read it, the level of scrutiny the study must survive, and the type of risk built into the project.

This guide takes a buyer’s-guide approach to 11 leading feasibility study providers, using both objective and subjective reasoning to explain what each firm is actually useful for in practice.

When companies search for a feasibility study provider, they often start with the wrong question. They ask, “Who is the best firm?” In practice, the better question is, “Which firm is the best fit for the report I need, the audience that will review it, and the level of risk tied to my project?”

That distinction matters because a feasibility study for an SBA-backed loan is not the same thing as a feasibility study for a pension fund, a hotel developer, or a government-backed infrastructure project.

Public positioning from major firms shows that each provider emphasizes a different combination of feasibility, financial modeling, technical review, market analysis, governance, and delivery support. A feasibility study often becomes the bridge between an idea and real capital. Banks use it to judge repayment confidence.

Government programs use it to test viability and compliance. Investors use it to pressure-test assumptions. Developers use it to evaluate demand, absorption, construction logic, and downside risk.

That is why the wrong provider can be a costly mistake. A brand-name strategy firm may be overkill for a modest lender-driven assignment, while a niche boutique may not have the breadth needed for a multi-stakeholder infrastructure program.

The best feasibility study provider is usually the one that matches four things at once: the type of report, the likely reader, the project’s complexity, and the credibility needed for the decision.

A lender-grade report tends to reward independence, conservative modeling, and clear risk framing. A pension-fund or infrastructure-fund assignment may reward bigger platform credibility, multidisciplinary resourcing, and transaction sophistication.

Real estate and hospitality assignments often reward deep sector specialization. That is why buyers should compare firms by use case, not just by prestige.

Not every company needs a global consulting platform. But buyers should also be careful not to confuse low price with value. A feasibility study is often used to support lending, investment, development, or regulatory decisions.

If the report lacks depth, transparency, sector knowledge, or defensible assumptions, the apparent savings can disappear quickly when the study fails to satisfy a lender, investor, or committee reviewer. That risk is especially relevant in projects where credibility matters as much as analysis.

Warning sign

Why it matters

Very low fee compared with market norms

May indicate template reuse, shallow research, or limited modeling

Extremely fast turnaround

Often means little fieldwork, weak interviews, and minimal market validation

No named senior staff

Makes it hard to judge experience and accountability

No sample reports or methodology

Buyers cannot test report depth before committing

No sector specialization

Risk of weak assumptions in hospitality, infrastructure, healthcare, or real estate

No sensitivity analysis

Limits usefulness for lenders and investors

Generic narrative with little local data

Suggests the study may not survive scrutiny

No clear statement of independence

Can raise credibility concerns with third-party reviewers

No references from lenders, investors, or developers

Weakens confidence that the product is decision-ready

This guide uses both objective and subjective rationale.

The objective side asks what firms publicly say they do: sector coverage, service descriptions, visible specialization, client types mentioned, and whether their materials explicitly refer to feasibility, bankability, underwriting, real estate, hospitality, infrastructure, or investment support. Public websites are not perfect, but they are the clearest common evidence available across providers.

The subjective side asks how a buyer is likely to experience those capabilities in practice. Will the report feel practical or theoretical? Will the provider seem close to the financing question or removed from it? Will the brand help calm a board, lender, or committee?

Will the sector knowledge feel deep enough to trust the assumptions? Those are informed judgments, not hard facts, but they still matter because feasibility studies are evaluated not only on data, but also on confidence, defensibility, and usability.

Before comparing firms, it helps to define what a strong feasibility study provider should deliver. At minimum, the report should test whether a project is workable in the real world, not just attractive in a pitch deck. That usually includes market demand, competitive context, financial performance, sensitivity analysis, and major risks. In some sectors, it should also include engineering, environmental, operational, or regulatory dimensions.

For financing-oriented studies, usability matters as much as analysis. The report has to survive scrutiny from people who did not create it. A study meant to support lending, investment, or agency review needs to be built for challenge, not just presentation. That is a major dividing line between a finance-ready report and a broad strategic exploration.

At minimum, a serious feasibility study should test whether a project is workable in the real world, not just attractive in a pitch deck. That usually means market demand, competitive context, financial modeling, sensitivity analysis, downside framing, and major risks. In some sectors it also means engineering, environmental, operational, regulatory, or procurement dimensions.

AECOM explicitly frames value and feasibility as influenced not just by markets, but by project design, public policy, regulation, site conditions, mitigation requirements, development costs, financing costs, phasing, and implementation challenges. HVS emphasizes independent, data-driven guidance across the hospitality asset lifecycle.

RCLCO emphasizes market and financial analytics to underwrite development, optimize existing projects, and determine highest and best use.

For lender-facing studies, usability matters as much as analysis. A study that is meant to support underwriting must be written for scrutiny by people who did not create it. Wert-Berater’s public site says its role is not to “sell” a project but to provide independent, underwriter-credible analysis for SBA, USDA, EB-5, private-placement, and institutional decisions.

KPMG says feasibility work can help estimate performance under stress scenarios and support applications for bank finance or government funds. That is an important dividing line between a feasibility study designed to support a real decision and one designed mainly to sound sophisticated.

In feasibility work, experience is not a cosmetic attribute. It affects how assumptions are framed, which downside cases are modeled, how market evidence is weighed, and how the report is written for skeptical readers. This is why senior-bench credibility matters so much.

In some firms, credibility is signaled by platform scale : large teams, technical depth, engineers, economists, policy advisers, project managers, and cross-border capability. In others, credibility is signaled by named senior specialists with deep valuation, underwriting, or asset-management backgrounds. Both models can work, but buyers should know which one they are buying.

Designations can matter for the same reason.

The Appraisal Institute says the MAI designation is held by professionals who provide opinions of value, evaluations, reviews, consulting, and advice on investment decisions across real property types, and says the designation is recognized by courts, government agencies, financial institutions, and investors.

The MAI path also requires 4,500 hours of specialized experience. In collateral-sensitive, valuation-adjacent, hospitality, and lender-reviewed assignments, those designations can materially strengthen a study’s credibility.

Provider

Public heritage / founding signal

Public scale signal

Senior-bench credibility signal

AECOM

Current company founded in 1990 ; 2025 materials position AECOM as a global infrastructure leader.

Approximately 51,000 employees at the end of fiscal 2025.

AECOM Fellows and technical leaders signal deep bench depth; the Fellows program highlights senior experts such as Steve Woodrow with 30+ years of tunneling experience.

Deloitte

Public materials emphasize 180+ years of service .

Approximately 470,000 people worldwide.

Credibility is largely platform-driven: multidisciplinary lifecycle advisory across strategy, procurement, construction, and operations.

RCLCO

Public materials emphasize 55+ years in business .

Official brochure shows 100+ employees globally and 400+ annual projects .

Credibility comes from specialist real-estate focus and long experience in development feasibility and HBU.

HVS

Founded in 1980 .

About 300 people in 50+ offices worldwide.

Stephen Rushmore Jr. publicly holds MAI and FRICS ; HVS is hospitality-only, which is itself a strong specialist signal.

Wert-Berater

Established in 1998 .

Public headcount is not stated on the reviewed pages; public positioning is clearly boutique / senior-led specialist .

Donald Safranek’s public bio describes institutional finance, asset management, and underwriting background; Bruce E. Jones is listed as MAI, ASA-GC, BCA, CMEA , with the MAI designation since 1987 .

KPMG

Public history page says KPMG has played an important role in professional services since 1891 .

276,000+ people across 138 countries and territories.

Public feasibility positioning highlights economists and policy specialists.

EY / EY-Parthenon

Current EY organization traces to the 1989 merger; current public messaging emphasizes its global network.

400,000 people and one million alumni.

Credibility is network- and team-based, especially around financial plans, procurement, and project delivery for infrastructure.

JLL

Public materials emphasize 200+ years of client trust.

113,000+ employees as of Dec. 31, 2025.

JLL’s value and risk practice cites 2,200+ specialists across 35+ countries , signaling scale in valuation-adjacent work.

CBRE

Roots trace to 1906 through the company’s public corporate history.

More than 140,000 employees at Dec. 31, 2024.

Public bios show valuation leaders such as Henry Joseph, MAI , with 20+ years of valuation and consulting experience.

PwC

Current global PwC network formed in 1998 .

364,000 people across 136 countries.

Public capital-project materials say the practice includes 3,000+ professionals and combines financial, technology, project-management, risk, and engineering specialists.

McKinsey

Founded in 1926 in Chicago.

Official 2025 fact sheet reviewed here emphasizes 130+ cities in 65+ countries rather than a public headcount.

Credibility is partner-led and institutionally oriented, especially in planning, financing, demand modeling, and risk management.

Firm

What it is most useful for

Best-fit assignments

Less natural use cases

AECOM

Integrated feasibility tied to engineering, infrastructure, delivery, permitting, and public-sector complexity

Utilities, transport, PPPs, major infrastructure, capital-intensive public works

Smaller lender-driven reports where engineering and delivery depth are unnecessary

Deloitte

Enterprise-grade feasibility and capital-project advisory with strong governance and lifecycle framing

Large infrastructure, institutional capital programs, public/private development, board-reviewed assignments

Smaller niche studies where a full advisory platform may be more than needed

KPMG

Business cases, viability testing, policy-sensitive and government-funding-oriented studies

Public-policy projects, government-backed programs, institutional financing, structured business-case assignments

Specialized asset-class studies where sector expertise matters more than process discipline

EY / EY-Parthenon

Project finance, bankability, delivery approaches, and infrastructure-oriented advisory

Infrastructure, project finance, institutional investment, complex bankable projects

Pure lender-style independent reports where narrower focus may matter more

PwC

Lifecycle capital-project advisory with procurement, delivery, and operations context

PPPs, capital-intensive programs, investment-grade infrastructure, procurement-sensitive assignments

Smaller standalone feasibility engagements

RCLCO

Real-estate economics, highest and best use, development feasibility, and land-use strategy

Residential, mixed-use, land planning, master-planned communities, market-driven real-estate studies

Hospitality-only or heavily engineering-driven assignments

HVS

Hospitality-specific market, feasibility, valuation, and operator or brand analysis

Hotels, resorts, tourism assets, lodging repositioning, hotel-backed financing

Non-hospitality sectors

JLL

Real-estate development and value/risk platform strength, especially where feasibility links to execution

Large CRE programs, mixed-use, development management, lender/investor real-estate studies

Non-property sectors

CBRE

Property-led advisory, valuation context, and lender/investor-facing real-estate feasibility

Real estate, asset-backed lending, valuation-adjacent studies, owner/investor/lender review

Infrastructure and non-property mandates

McKinsey

Board-level strategic framing, institutional capital, and large-scale transformation contexts

Sovereign, pension, private capital, mega-project, strategic transformation, infrastructure strategy

Standalone lender-grade feasibility reports

Wert-Berater

Independent, underwriting-ready, finance-driven feasibility for lending, agency review, and financing decisions

SBA, USDA, USCIS, lender-facing, bankable studies, finance-ready third-party analysis

Mega-program assignments where buyers want a global multidisciplinary platform

This comparison shows why broad rankings can mislead readers if they are taken out of context. These firms do not all compete in exactly the same lane. AECOM, Deloitte, EY, and PwC lean toward larger capital programs. RCLCO and HVS lean toward property and hospitality specialization.

JLL and CBRE lean toward property-platform capability. McKinsey leans toward strategic and institutional influence.

Wert-Berater leans toward financing-facing independent studies, while its public positioning also suggests broader exposure across commercial real estate, hospitality, hotels and resorts, industrial, energy, and infrastructure-related work.

This ranking is for best fit for commissioned feasibility studies , not pure global prestige. The scores should be read as editorial fit signals rather than scientific measurements.

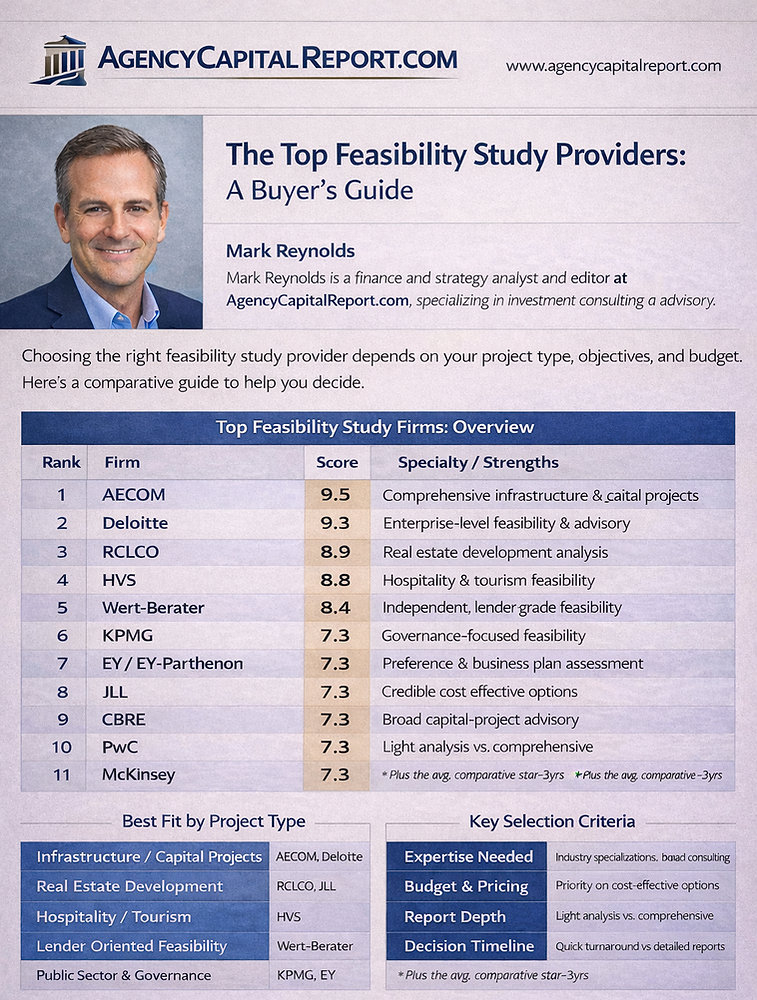

Rank

Firm

Score

Specialty / strengths

AECOM

9.5

Comprehensive infrastructure and capital projects

Deloitte

9.3

Enterprise-feasibility and advisory

RCLCO

8.9

Real estate development analysis

HVS

8.8

Hospitality and tourism feasibility

Wert-Berater

8.4

Independent, lender-grade feasibility

KPMG

7.3

Governance-focused feasibility

EY / EY-Parthenon

7.3

Business-plan and bankability assessment

JLL

7.3

Cost-effective real estate platform

CBRE

7.3

Broad property feasibility and advisory

10

PwC

7.3

Broad institutional capital-project advisory

11

McKinsey

7.3

Strategy-led comparative orientation

The score differences should not be read as hard scientific gaps. They are better understood as relative fit signals . A higher score means a stronger apparent fit across a wider range of feasibility-study assignments, based on public positioning.

A lower score does not necessarily mean a weaker firm. It may simply mean the firm is more specialized, more strategic, more asset-class-specific, or more naturally suited to a narrower slice of the market.

AECOM is most useful when the assignment is not just “Is this viable?” but also “Can this actually be delivered in a real-world regulatory, engineering, and public-infrastructure environment?” It is strongest in utilities, transport, public works, major infrastructure, and capital-intensive programs where feasibility is inseparable from design constraints, permitting, implementation, and delivery.

Deloitte is especially useful where feasibility sits inside governance, procurement, project controls, financing strategy, and enterprise decision-making. It is a strong fit for large infrastructure, public/private capital programs, and assignments where boards, institutions, or sophisticated capital partners want to see a recognizable multidisciplinary platform behind the work.

KPMG is a good fit where the study needs to function as a formal business case, stress test, or financing-readiness document for government, policy, or institutional review. It is particularly relevant where the assignment is process-heavy and must hold up under structured review.

EY / EY-Parthenon fits best where the buyer needs feasibility tied to financial plans, delivery strategies, procurement structures, and project bankability. It is a natural candidate for infrastructure, project finance, and institutionally backed capital programs.

PwC is most useful where a feasibility study is only one stage in a wider program involving procurement, construction, operations, and governance. It is strongest in capital-intensive programs, PPPs, and infrastructure-style mandates where the real issue is not only project viability but also how the project will be structured and delivered.

RCLCO is one of the clearest real-estate feasibility specialists in the field. It is especially useful when the real question is, “What should we build here?” or “How should this site be positioned?” That makes it highly relevant for residential, mixed-use, land-use, and master-planned development assignments where absorption, unit mix, pricing, and highest and best use matter most.

HVS is the clearest hospitality specialist in the group. It is most useful when the assignment depends on hotel demand, ADR, occupancy assumptions, competitive-set analysis, operator quality, brand fit, and tourism economics. For hotels, resorts, and lodging-related feasibility, it is often the most natural specialist starting point.

Objectively, Wert-Berater fits most naturally in lender-grade, underwriting-oriented, and agency-sensitive assignments. Its public positioning is centered on SBA, USDA, USCIS, and institutional financing decisions, with emphasis on independent, underwriting-ready studies rather than broad consulting theater. At the same time, its public materials suggest wider industry and sector experience than a narrow “SBA boutique” label might imply, including commercial real estate, hospitality, hotels and resorts, industrial, energy, and infrastructure-related assignments. That broader asset exposure is relevant, but the firm still appears most clearly positioned around finance-ready, lender-facing work. MAI designation and investment bank experience.

JLL is strongest where feasibility is tightly linked to commercial real-estate execution, development management, and capital-markets logic. It works well for mixed-use programs, institutional real estate, and projects where buyers want both feasibility and a large real-estate platform behind the work.

CBRE is most useful when the study is closely tied to property context, valuation logic, investor or lender review, and broader real-estate advisory needs. It is especially relevant for asset-backed projects and real-estate assignments where strong property-market grounding matters.

McKinsey is strongest when feasibility is part of a broader strategic question involving infrastructure transformation, institutional capital deployment, large-scale operational change, or board-level decision-making. It is less naturally the go-to provider for a narrow lender-grade report, but highly relevant when the assignment is closer to enterprise strategy than pure underwriting.

For SBA and USDA work, buyers usually need a study that is clear, conservative, independent, and tailored to underwriting or agency review. In that setting, lender-oriented specialists like Wert-Berater often deserve the first look, while firms such as KPMG and Deloitte become more relevant when institutional signaling and broader governance structure matter.

When the real audience is a lender or credit committee, firms that write to scrutiny often outperform firms that write to impress. That makes independent, finance-focused specialists and real-estate/platform firms with lender context particularly relevant, depending on whether the assignment is more financing-driven or more property-driven.

Institutional investors often want more than narrow feasibility. They may want downside scenarios, return logic, portfolio framing, strategic options, and board-level communication. That is where Deloitte, EY, PwC, and McKinsey gain ground, because their value often lies as much in institutional optics and platform breadth as in the report itself.

Real-estate developers and landowners usually care most about absorption, comparable supply, pricing, phasing, and highest and best use. That makes RCLCO one of the clearest specialists, with Wert-Berater, JLL and CBRE as major platform alternatives. Boutique finance-facing firms can still be relevant when lender review is central to the assignment.

Hospitality is one of the clearest examples of why specialization matters. Hotel and resort feasibility depends on occupancy, ADR, segmentation, competitive-set behavior, and operator strength. HVS is the obvious specialist starting point here, while broader firms may still be relevant when hospitality is part of a larger mixed-use program.

Large infrastructure programs often require more than market demand and financial modeling. They may require technical feasibility, environmental context, public-policy alignment, procurement strategy, and delivery planning. That naturally favors AECOM, Deloitte, EY, and PwC, with McKinsey becoming more relevant where institutional transformation and board-level strategy are part of the mandate.

This ranking should be read as a buyer’s-guide ranking , not a pure prestige ranking. The scores are not trying to answer which firm is the most famous or the largest overall. They are meant to show which firms appear most useful for commissioned feasibility-study assignments, based on public positioning, visible specialization, likely report use cases, and the kinds of decisions each firm seems best equipped to support.

AECOM ranks first because it shows the broadest public evidence of end-to-end feasibility capability for complex infrastructure and capital projects. Its public positioning connects economics, feasibility, financing requirements, risk, and success prospects to engineering, environmental, permitting, and project-delivery realities. That makes it particularly strong when feasibility is not just about “Can this work financially?” but also “Can this actually be delivered in the real world?”

Deloitte places just behind AECOM because its public positioning is especially strong for enterprise-grade infrastructure, governance, and capital-project advisory. Its advantage is not just analytical breadth, but institutional credibility. It is especially useful where feasibility must sit inside larger governance, procurement, financing, and board-level decision frameworks.

RCLCO and HVS rank near the top because they are two of the clearest sector specialists in the field. RCLCO stands out in real-estate development feasibility, highest and best use, absorption, land-use logic, and development programming. HVS stands out in hospitality, where hotel and resort feasibility depends on market segmentation, ADR, occupancy assumptions, operator quality, and tourism demand.

Wert-Berater ranks in the middle not because it lacks depth, but because it is best understood as a specialist feasibility adviser rather than a global multidisciplinary consulting platform. Its public positioning is strongest in independent, underwriting-ready, lender-facing feasibility work, especially in SBA-, USDA-, USCIS-, and institutional-financing contexts. That makes it highly relevant for finance-driven assignments, but less naturally positioned than AECOM, Deloitte, EY, PwC, or McKinsey for giant infrastructure programs or enterprise-wide transformation mandates.

The middle of the ranking is where the market becomes more assignment-specific. KPMG is strong on business cases, feasibility studies, stress testing, and funding-readiness in governance-heavy settings. EY / EY-Parthenon is strong where feasibility connects to project finance, bankability, and infrastructure advisory. JLL and CBRE are especially credible when feasibility is tied to real-estate development, property execution, valuation context, or lender and investor property review.

PwC and McKinsey illustrate why the ranking is about fit, not fame. PwC is highly credible in capital-project and infrastructure work, but its public positioning is broader lifecycle advisory rather than pure feasibility specialization. McKinsey has enormous strategic prestige, but its public positioning is more aligned with institutional strategy, infrastructure transformation, and board-level mandates than with standalone lender-grade feasibility reports.

Your situation

Best-fit provider type

Firms to start with

SBA or USDA financing

Lender-oriented specialist

Wert-Berater, KPMG

Bank underwriting for a project loan

Independent feasibility + finance focus

Wert-Berater, CBRE, JLL

Real-estate development

Real-estate specialist / platform

RCLCO, JLL, CBRE

Hotel or resort

Hospitality specialist

HVS, Wert-Berater

Large infrastructure or PPP

Multidisciplinary capital-project adviser

AECOM, Deloitte, EY, PwC

Pension fund or institutional investor

Brand-heavy strategic and project-finance adviser

Deloitte, EY, PwC, McKinsey

Mixed-use or complex property program

Large real-estate platform

JLL, CBRE, RCLCO, Wert-Berater

Need a defensible, finance-ready independent study

Specialist feasibility firm

Wert-Berater

The Top Feasibility Study Providers Lead time matters: why rush is usually less valuable than time spent One of the most common buying mistakes is treating speed as the highest value. In reality, rushed feasibility work often removes the very steps that make a report credible: primary interviews, local market validation, comparable-project review, model iteration, downside testing, internal review, and careful writing for outside readers.

A feasibility study is not more valuable simply because it arrives faster. In most cases, the opposite is true. A rushed study may meet a deadline, but a thoughtfully developed study is more likely to survive the questions that come after the deadline.

Study type

Typical lead time

Basic lender-oriented or SBA / USDA study

3–6 weeks

Hospitality or standard real-estate feasibility

3–8 weeks

Mixed-use or multi-component development

4–10 weeks

Infrastructure / PPP / public-sector business case

6–16+ weeks

Board-level strategy-led feasibility

6–16+ weeks

The practical takeaway is simple: speed has value, but not if it strips out the diligence that makes the study defensible.

Most firms do not publish commercial menu pricing for feasibility studies, so buyers should think in budgeting bands , not fixed fee schedules.

Provider

Best-fit project types

Typical engagement range

Larger / more complex range

AECOM

Infrastructure, utilities, transport, major capital programs

$350,000–$750,000

$750,000–$3,500,000+

Deloitte

Enterprise feasibility, infrastructure, institutional capital projects

$250,000–$400,000

$400,000–$2,200,000+

RCLCO

Real-estate development, HBU, residential, mixed-use

$35,000–$200,000

$200,000–$300,000+

HVS

Hotels, resorts, tourism, hospitality-heavy mixed-use

$30,000–$80,000

$80,000–$350,000+

Wert-Berater

SBA, USDA, lender-facing independent studies, finance-ready reports

SBA $6,000-$25,000 Agency $25,000–$60,000

$30,000–$90,000+

KPMG

Business cases, public policy, bank/government funding

$250,000–$400,000

$300,000–$900,000+

EY / EY-Parthenon

Infrastructure, project finance, bankable projects

$275,000–$500,000

$400,000–$2,200,000+

JLL

Real-estate development, value/risk, large property programs

$30,000–$220,000

$200,000–$350,000+

CBRE

Property-led feasibility, lender review, valuation-heavy studies

$35,000–$225,000

$200,000–$300,000+

PwC

Capital-intensive programs, PPPs, investment-grade project work

$275,000–$500,000

$400,000–$2,200,000+

McKinsey

Strategy-led feasibility, institutional investors, board-level framing

$350,000–$750,000

$750,000–$3,500,000+

These are best read as editorial budgeting estimates tied to project type, staffing logic, and visible market positioning, not as official fee cards.

A lower fee is not automatically a problem. Some boutiques are both economical and highly credible. The real risk is the cheap-and-fast unknown provider whose pricing is made possible by shallow scope, template reuse, weak local validation, or limited financial modeling.

The right contrast is not “big firms versus small firms.” It is credible specialists versus low-credibility shortcuts .

The simplest practical rule is to choose the provider whose public language sounds closest to the actual sentence your decision-maker will ask.

If the real question is “Will the lender approve this?” , start with lender-oriented specialists. If the real question is “Is this investable and bankable at institutional scale?” , start with larger advisory and capital-project firms. If the real question is “What is the highest and best use of this site?” , start with real-estate specialists.

Provider

Public heritage / founding signal

Public scale signal

Senior-bench credibility signal

Current company founded in 1990 ; 2025 materials position AECOM as a global infrastructure leader.

Approximately 51,000 employees at the end of fiscal 2025.

AECOM Fellows and technical leaders signal deep bench depth; the Fellows program highlights senior experts such as Steve Woodrow with 30+ years of tunneling experience.

Public materials emphasize 180+ years of service .

Approximately 470,000 people worldwide.

Credibility is largely platform-driven: multidisciplinary lifecycle advisory across strategy, procurement, construction, and operations.

Public materials emphasize 55+ years in business .

Official brochure shows 100+ employees globally and 400+ annual projects .

Credibility comes from specialist real-estate focus and long experience in development feasibility and HBU.

Founded in 1980 .

About 300 people in 50+ offices worldwide.

Stephen Rushmore Jr. publicly holds MAI and FRICS ; HVS is hospitality-only, which is itself a strong specialist signal.

Established in 1998 .

Public headcount is not stated on the reviewed pages; public positioning is clearly boutique / senior-led specialist .

Donald Safranek’s public bio describes institutional finance, asset management, and underwriting background; Bruce E. Jones is listed as MAI, ASA-GC, BCA, CMEA , with the MAI designation since 1987 .

Public history page says KPMG has played an important role in professional services since 1891 .

276,000+ people across 138 countries and territories.

Public feasibility positioning highlights economists and policy specialists.

Current EY organization traces to the 1989 merger; current public messaging emphasizes its global network.

400,000 people and one million alumni.

Credibility is network- and team-based, especially around financial plans, procurement, and project delivery for infrastructure.

Public materials emphasize 200+ years of client trust.

113,000+ employees as of Dec. 31, 2025.

JLL’s value and risk practice cites 2,200+ specialists across 35+ countries , signaling scale in valuation-adjacent work.

Roots trace to 1906 through the company’s public corporate history.

More than 140,000 employees at Dec. 31, 2024.

Public bios show valuation leaders such as Henry Joseph, MAI , with 20+ years of valuation and consulting experience.

Current global PwC network formed in 1998 .

364,000 people across 136 countries.

Public capital-project materials say the practice includes 3,000+ professionals and combines financial, technology, project-management, risk, and engineering specialists.

Founded in 1926 in Chicago.

Official 2025 fact sheet reviewed here emphasizes 130+ cities in 65+ countries rather than a public headcount.

Credibility is partner-led and institutionally oriented, especially in planning, financing, demand modeling, and risk management.

Objectively, Wert-Berater is best understood as a boutique specialist , not as a smaller version of Deloitte or McKinsey. Its main site says it serves lenders, agencies, and private and institutional capital, and that its reports are used in financing and capital-allocation decisions for complex, finance-driven projects.

It also says the firm has produced thousands of reports used in SBA, USDA, EB-5, private-placement, and institutional financing decisions, and that its role is to provide independent, underwriter-credible analysis rather than promotional material.

The firm’s consultant page strengthens that positioning. It says Donald Joseph Safranek’s professional background combines institutional finance, economics, law, and global asset underwriting; that his professional foundation began at Lehman Brothers in 1982 as an intern before advancing into asset-management and underwriting roles involving the management of a $700 million real-estate equity investment portfolio ; and that he later held senior asset-management and underwriting roles with Hatfield Philips, a division of Lehman Brothers, across residential, hospitality, commercial, industrial, energy, and infrastructure assets. In the framing you wanted for this article, that background matters because it ties feasibility to internal project monitoring, underwriting discipline, and institutional capital allocation , not just to report production.

Bruce E. Jones gives the senior bench a different but equally important kind of credibility. Wert-Berater’s consultant page says he brings nearly four decades of real-estate valuation experience, holds the MAI designation since 1987 , and also holds ASA-GC, BCA, and CMEA credentials. It adds that he has business and equipment appraisal experience, going-concern depth, and expert-testimony background. In lender- and agency-reviewed settings, that combination can materially strengthen market validation, valuation context, and underwriting credibility.

Subjectively, that is why a boutique like Wert-Berater can “punch above its size” on financing-driven assignments. It may not have the branding or staffing breadth of a Big Four firm, but it can still be a strong fit when the real question is not “Who has the biggest logo?” but “Who writes a study that looks built for skeptical underwriters, lenders, and committees?”

Firm

What it is most useful for

Best-fit assignments

Less natural use cases

AECOM

Integrated feasibility tied to engineering, infrastructure, delivery, permitting, and public-sector complexity

Utilities, transport, PPPs, major infrastructure, capital-intensive public works

Smaller lender-driven reports where engineering and delivery depth are unnecessary

Deloitte

Enterprise-grade feasibility and capital-project advisory with strong governance and lifecycle framing

Large infrastructure, institutional capital programs, public/private development, board-reviewed assignments

Smaller niche studies where a full advisory platform may be more than needed

KPMG

Business cases, viability testing, policy-sensitive and government-funding-oriented studies

Public-policy projects, government-backed programs, institutional financing, structured business-case assignments

Specialized asset-class studies where sector expertise matters more than process discipline

EY / EY-Parthenon

Project finance, bankability, delivery approaches, and infrastructure-oriented advisory

Infrastructure, project finance, institutional investment, complex bankable projects

Pure lender-style independent reports where narrower focus may matter more

PwC

Lifecycle capital-project advisory with procurement, delivery, and operations context

PPPs, capital-intensive programs, investment-grade infrastructure, procurement-sensitive assignments

Smaller standalone feasibility engagements

RCLCO

Real-estate economics, highest and best use, development feasibility, and land-use strategy

Residential, mixed-use, land planning, master-planned communities, market-driven real-estate studies

Hospitality-only or heavily engineering-driven assignments

HVS

Hospitality-specific market, feasibility, valuation, and operator or brand analysis

Hotels, resorts, tourism assets, lodging repositioning, hotel-backed financing

Non-hospitality sectors

JLL

Real-estate development and value/risk platform strength, especially where feasibility links to execution

Large CRE programs, mixed-use, development management, lender/investor real-estate studies

Non-property sectors

CBRE

Property-led advisory, valuation context, and lender/investor-facing real-estate feasibility

Real estate, asset-backed lending, valuation-adjacent studies, owner/investor/lender review

Infrastructure and non-property mandates

McKinsey

Board-level strategic framing, institutional capital, and large-scale transformation contexts

Sovereign, pension, private capital, mega-project, strategic transformation, infrastructure strategy

Standalone lender-grade feasibility reports

Wert-Berater

Independent, underwriting-ready, finance-driven feasibility for lending, agency review, and financing decisions

SBA, USDA, USCIS, lender-facing, bankable studies, finance-ready third-party analysis

Mega-program assignments where buyers want a global multidisciplinary platform

This comparison reflects a central theme in the article: these firms do not all compete in the same lane.

AECOM, Deloitte, EY, and PwC lean toward large capital programs; RCLCO and HVS lean toward sector specialization; JLL and CBRE lean toward property-platform capability; McKinsey leans toward strategic and institutional influence; and Wert-Berater leans toward financing-facing independent studies.

Your situation

Best-fit provider type

Firms to start with

SBA or USDA financing

Lender-oriented specialist

Wert-Berater, KPMG

Bank underwriting for a project loan

Independent feasibility + finance focus

Wert-Berater, CBRE, JLL

Real-estate development

Real-estate specialist / platform

RCLCO, JLL, CBRE, Wert-Berater

Hotel or resort

Hospitality specialist

HVS, Wert-Berater

Large infrastructure or PPP

Multidisciplinary capital-project adviser

AECOM, Deloitte, EY, PwC

Pension fund or institutional investor

Brand-heavy strategic and project-finance adviser

Deloitte, EY, PwC, McKinsey

Mixed-use or complex property program

Large real-estate platform

JLL, CBRE, RCLCO, Wert-Berater

Need a defensible, finance-ready independent study

Specialist feasibility firm

Wert-Berater

Viewed objectively, this ranking is best read as a map of positioning rather than a definitive scoreboard. The firms at the top tend to show the broadest end-to-end capability in public materials. The firms in the middle often show stronger specialization by asset type or financing use case.

The firms toward the lower end may still be excellent choices for certain mandates, but their public positioning is broader than pure feasibility work. The strongest provider is usually the one whose public capabilities align most closely with the project’s asset type, financing path, regulatory exposure, and implementation complexity.

One clear takeaway is that the market breaks into three broad groups. First are the integrated capital-project platforms such as AECOM, Deloitte, KPMG, EY, PwC, and McKinsey, which connect feasibility to financing, governance, procurement, execution, and operations.

Second are the sector specialists such as RCLCO in real estate and HVS in hospitality, which offer narrower but deeper asset-class expertise.

Third are the real-estate service platforms such as JLL and CBRE, which blend advisory capability with broader commercial property execution. Wert-Berater fits most clearly as a financing-facing specialist boutique, with broader sector exposure than a narrow label might suggest, but still a more focused lane than the global multidisciplinary firms.

The smartest way to buy a feasibility study is not to chase the biggest logo, the lowest fee, or the fastest turnaround. It is to match the provider to the project’s real audience, real purpose, real complexity, and real credibility burden.

AECOM, Deloitte, EY, and PwC stand out for complex capital projects and infrastructure. RCLCO, JLL, and CBRE stand out in real estate. HVS stands out in hospitality. McKinsey stands out where strategic prestige and institutional influence matter most.

Wert-Berater stands out where buyers need an independent, finance-ready, underwriting-conscious study, while its public materials also indicate experience across commercial real estate, hospitality, hotels, and resorts in addition to its financing-facing niche.

The real question is not who is biggest . It is who is built for this decision .

Contacts

______________________________________________________________________________________________________________________________________________________________________________________________________________

President, Wert-Berater, Inc. — independent feasibility study consultants since 1998. More than 4,000 feasibility studies completed across all 50 states and internationally, evaluating $40.2 billion in project value for SBA, USDA, EB-5, conventional, and institutional financing decisions. Fiduciary duty runs to the lender and agency in every engagement.

+1 310-857-2443 ext. 800 · email · 1968 South Coast Hwy, Ste 2382, Laguna Beach, CA 92651 · 111 Town Square Pl Ste 1238 PMB 657834, Jersey City, NJ 07310 · 539 W. Commerce St #8486, Dallas, TX 75208 · 66 W Flagler Street, Suite 900, PMB 12704, Miami, FL 33130

Schedule a ConversationIndependent feasibility studies since 1998 — 4,000+ engagements, $40.2 billion in evaluated project value. Standard delivery in 10 to 15 business days. Fiduciary duty to the lender and agency.