Palm Beach County’s ambulatory surgery center market is supported by strong demographics and outpatient growth, but it is already highly competitive. This analysis examines 41 identified facilities, hospital financial performance, service gaps, and the most supportable opportunities for new centers, expansions, acquisitions, and physician-aligned joint ventures.

Evaluating a surgery center project? See our ambulatory surgery center feasibility studies — independent, lender-grade analysis for physician owners, health systems, investors, and lenders.

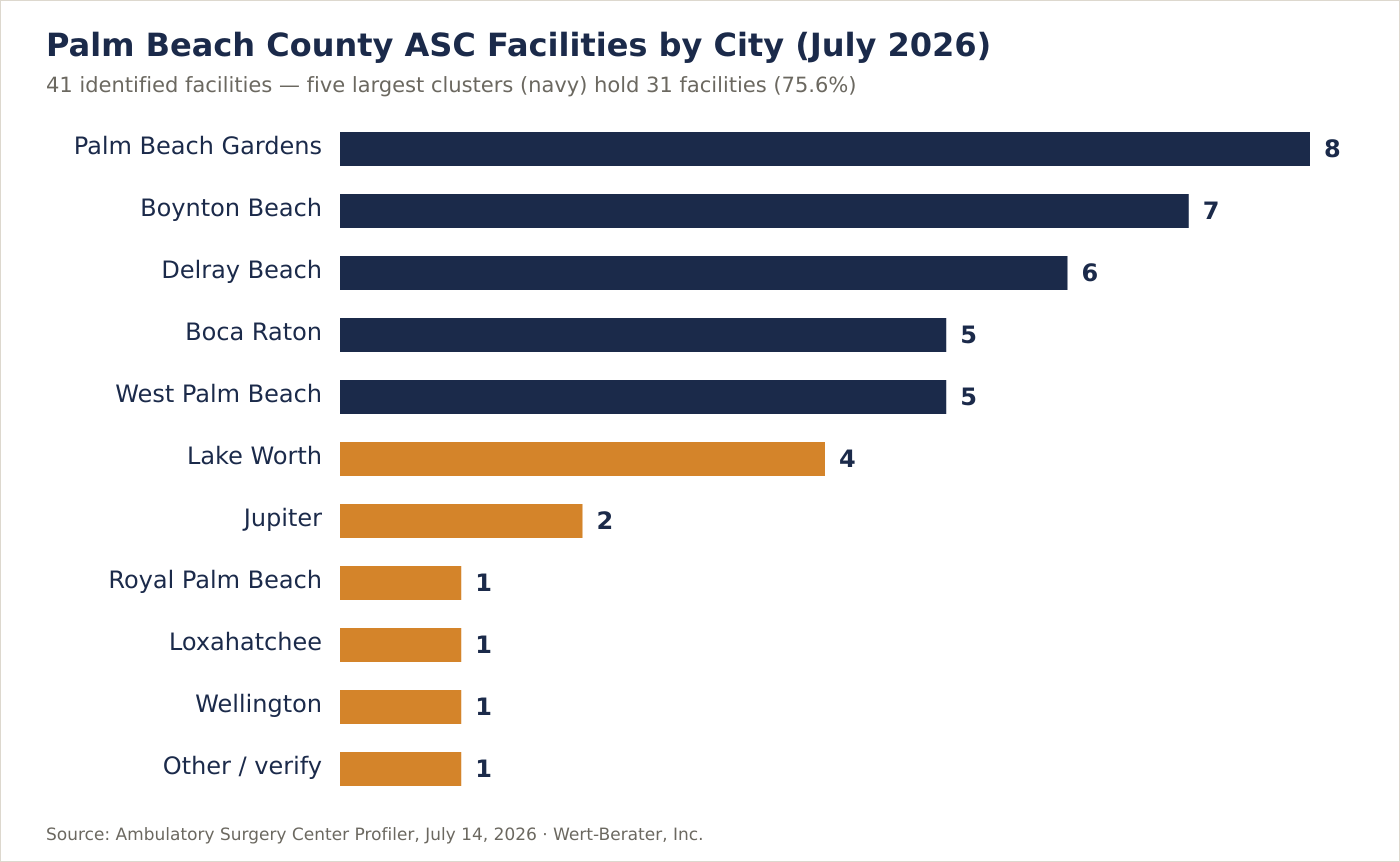

Palm Beach County’s ambulatory surgery center market is financially active, demographically favorable, and increasingly competitive. The July 2026 market dataset identifies 41 facilities, including 39 centers with CMS certification numbers. Approximately 75.6% of the identified facilities are concentrated in Palm Beach Gardens, Boynton Beach, Delray Beach, Boca Raton, and West Palm Beach.

Demand remains supported by an estimated 1.58 million county residents, approximately 411,000 people age 65 or older, and continued migration of appropriate surgical procedures from hospital inpatient and outpatient departments into lower-cost ambulatory settings.

The Palm Beach County ASC market is not uniformly underserved. Countywide facility density is relatively high, but targeted opportunities may exist in western Palm Beach County, the Jupiter and north-county corridor, orthopedic and total-joint services, selected spine procedures, cardiovascular care, and strategic expansion of high-performing existing centers.

Key finding: Palm Beach County appears better suited to targeted ASC expansion, physician-aligned joint ventures, and specialty or geographic gap strategies than to an undifferentiated greenfield multispecialty facility.

| Indicator | Market result |

|---|---|

| Identified ASC facilities | 41 |

| Facilities with CMS certification numbers | 39 |

| Facilities in five largest clusters | 31 |

| Share in five largest clusters | 75.6% |

| Estimated county population | 1.58 million |

| Residents age 65 or older | ≈411,000 (26.1%) |

| Median household income | ≈$83,600 |

| Medicare-certified ASCs per 100,000 residents | ≈2.48 |

As a rough density screen, Palm Beach County has approximately 31% more Medicare-certified ASCs per resident than the national level of about 1.89 per 100,000. This is not a capacity study — the comparison uses different reporting dates and does not account for operating rooms, hours, specialties, case volume, or catchment overlap — but it signals that Palm Beach County is not an obvious undersupplied market at the countywide level.

The Palm Beach County ASC market is healthy from a demand and outpatient-growth perspective, but mature from a competitive-supply perspective.

Six forces define the market’s condition: demographic strength, outpatient procedure migration, a moderately positive reimbursement environment, existing facility density, wide variation in hospital financial health, and accelerating physician alignment and consolidation. Each is examined below.

The broader ASC industry continues to expand. MedPAC reported 6,436 Medicare-certified ASCs in 2024, up 2.2% from 2023. During that year, 248 facilities opened and 108 closed or merged, creating a net increase of 140 facilities. Approximately 95.3% of ASCs were for-profit.

Demand and reimbursement indicators were also positive:

CMS also increased qualifying ASC payment rates by 2.6% for 2026. The 2026 policy environment expands the outpatient opportunity further: CMS began phasing out the inpatient-only list and added hundreds of procedures to the ASC covered-procedure list, including musculoskeletal, spinal, laparoscopic, and cardiovascular procedures.

These trends support long-term outpatient migration, but they do not guarantee that every new center will succeed. National growth is occurring alongside consolidation, physician alignment, payer pressure, and increasing specialization.

Local supply is heavily concentrated in the eastern population corridor. The 41 facilities in the dataset are distributed as follows:

| City or submarket | Facilities | Share |

|---|---|---|

| Palm Beach Gardens | 8 | 19.5% |

| Boynton Beach | 7 | 17.1% |

| Delray Beach | 6 | 14.6% |

| Boca Raton | 5 | 12.2% |

| West Palm Beach | 5 | 12.2% |

| Lake Worth | 4 | 9.8% |

| Jupiter | 2 | 4.9% |

| Royal Palm Beach | 1 | 2.4% |

| Loxahatchee | 1 | 2.4% |

| Wellington | 1 | 2.4% |

| Other or location requiring verification | 1 | 2.4% |

The five largest clusters contain 31 of the 41 facilities. This suggests that the east-coast population corridor has considerable provider choice, while north-county and western communities may offer more targeted access opportunities.

The dataset also contains data-quality issues that should be resolved before a final market conclusion. One provider is shown in Winter Park with a Palm Beach County ZIP code, several city names require normalization, and two providers lack CMS certification numbers. Facility addresses should be geocoded and matched against current Florida AHCA licenses.

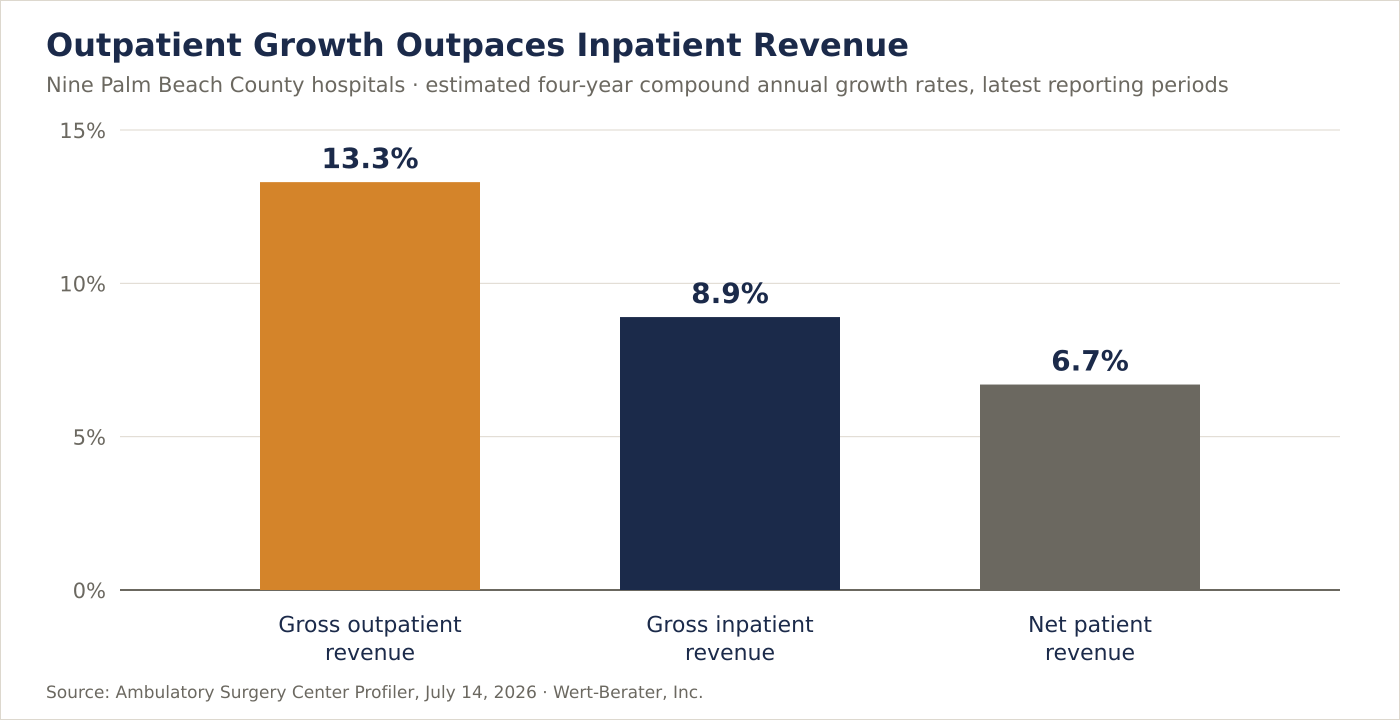

The dataset includes full financial statements for nine acute-care hospitals serving Palm Beach County. Based on each hospital’s latest available reporting period, generally ending in 2024 or 2025, these hospitals collectively reported:

| Aggregate acute-hospital indicator | Latest result |

|---|---|

| Net patient revenue | $3.93 billion |

| Operating income | $348.8 million |

| Weighted operating margin | 8.9% |

| Net income | $477.2 million |

| Aggregate current ratio | 1.54x |

| Gross billed outpatient revenue | $14.40 billion |

| Gross billed inpatient revenue | $20.41 billion |

| Outpatient share of gross patient revenue | 41.4% |

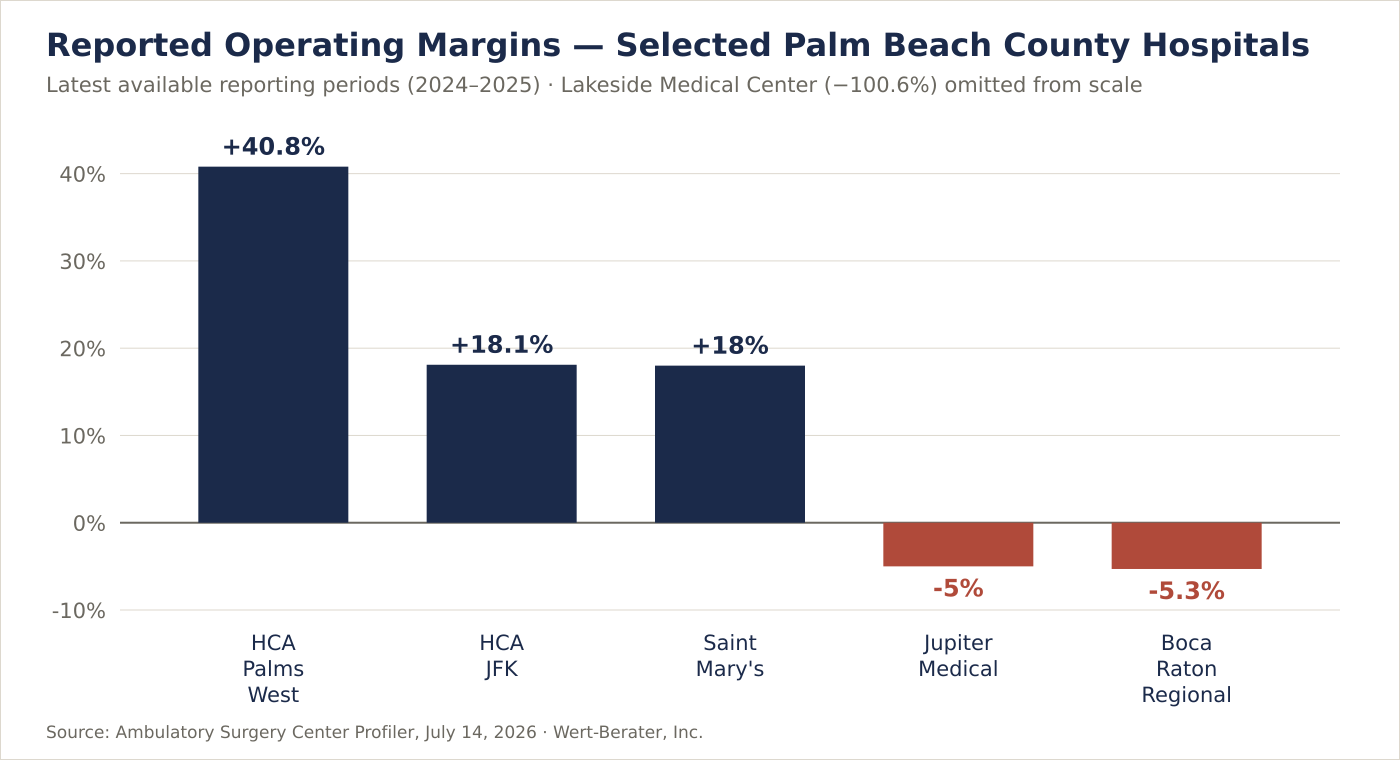

| Hospitals with positive operating margins | 6 of 9 |

The most important trend is the continued shift toward outpatient activity. Across the nine hospitals:

This is a strong directional indicator of outpatient demand and site-of-care migration.

The top acute-hospital operating margins were HCA Florida Palms West Hospital at 40.8%, HCA Florida JFK Hospital at 18.1%, and Saint Mary’s Medical Center at 18.0%. Other positive-margin hospitals included Palm Beach Gardens Medical Center, Delray Medical Center, and Good Samaritan Medical Center, each near 9% to 10%.

The weakest results were Lakeside Medical Center at –100.6%, Boca Raton Regional Hospital at –5.3%, and Jupiter Medical Center at –5.0%.

Lakeside’s result should not be read as a normal commercial-provider benchmark. Its public-service role, payer mix, cost-report structure, and nonpatient support materially affect its economics. It nevertheless illustrates the financial challenge of serving western or safety-net markets solely through conventional volume and payer assumptions.

Boca Raton Regional Hospital and Jupiter Medical Center are particularly interesting strategically. Both had negative operating margins but high outpatient exposure:

Those figures may support hospital–physician joint ventures, off-campus rationalization, or migration of appropriate cases to a lower-cost setting. They do not prove that a new facility is required; a feasibility study must determine whether incremental ASC contribution margin would exceed the hospital revenue displaced.

A separate financial-indicator sheet shows Bethesda Hospital East improving from a –36.3% operating margin in 2022 to –9.9% in 2025. EBITDAR turned positive at approximately $3.5 million, and personnel expense fell from 72.0% to 48.8% of operating revenue.

The remaining indicators are still concerning: a 1.0x current ratio, a 0.9x quick ratio, 2.5 days cash on hand from all sources, a 61.1-day average payment period, total liabilities of approximately $777.9 million, and total assets of approximately $453.7 million. Because net assets are negative, the reported return-on-equity and debt-to-net-assets ratios are not economically meaningful. The more useful conclusion is that operations are improving, but liquidity and balance-sheet pressure remain material.

This is likely the lowest-risk opportunity. A center with an established surgeon roster, payer contracts, demonstrated utilization, and physical expansion capacity has advantages over a greenfield project. Expansion could involve adding an operating or procedure room, extending operating hours, adding higher-acuity cases, introducing a complementary specialty, expanding recovery capacity, or improving block-time utilization.

The key is to establish whether existing rooms are truly capacity constrained. An expansion is not warranted merely because annual cases are growing; weekday and hourly utilization, turnover time, cancellation rates, and surgeon backlog must be evaluated.

This is one of the clearest growth sectors nationally. Total hip and knee volumes are increasing rapidly, and 2026 reimbursement policy expands the number of musculoskeletal and spinal procedures that can potentially migrate to ASCs. Single-specialty orthopedic centers increased 18.9% nationally from 2023 to 2024, while multispecialty centers combining pain management and orthopedics increased 20.9%.

Palm Beach County’s age profile supports orthopedic demand, but competition is already substantial. The market includes HSS, the Paley Institute, orthopedic surgery centers, pain centers, and hospital-affiliated programs. The more credible strategies are therefore expansion of an existing orthopedic center, a physician-anchored joint venture, addition of total-joint capacity to an established multispecialty facility, or a hospital partnership designed to move appropriate cases out of a hospital outpatient department. A speculative orthopedic center without committed surgeons would carry high risk.

Cardiology was among the fastest-growing single-specialty ASC categories nationally, with facility count increasing 6.3% in one year. The 2026 covered-procedure expansion also included several cardiovascular procedures. The local facility names do not reveal a clearly dominant dedicated cardiovascular ASC category. That may represent an opportunity, but facility names are not a reliable service inventory.

A cardiovascular concept should advance only after confirming cardiologist and vascular-surgeon commitments, current hospital and office-based laboratory volumes, state licensure and life-safety requirements, transfer arrangements, implant and supply costs, commercial and Medicare reimbursement, patient-selection protocols, and case-acuity limits.

Only two facilities in the dataset are listed in Jupiter, compared with eight in Palm Beach Gardens. Jupiter has approximately 63,000 residents, a median household income above $110,000, and approximately 24.4% of residents age 65 or older. Jupiter Medical Center’s outpatient gross revenue also grew approximately 18.6% annually in the dataset.

This creates a plausible north-county opportunity, but Palm Beach Gardens centers may already draw significantly from Jupiter. A drive-time and patient-origin analysis is required before declaring a geographic gap.

The dataset lists only one facility in each of these western communities. Wellington alone has approximately 62,700 residents, median household income of about $115,600, and an average commute of more than 32 minutes. This corridor may support a focused ASC or expansion, especially where patients currently travel east for treatment.

The western opportunity also carries higher uncertainty. Lakeside Medical Center’s financial performance suggests that the far-western market may face lower commercial-payer density, greater uncompensated-care exposure, and insufficient volume for a large multispecialty greenfield facility. A smaller specialty-focused center, hospital partnership, or phased project may be more defensible than a broad facility.

Gastroenterology and ophthalmology remain the two largest ASC specialties nationally, representing about 21% and 20% of ASCs billing Medicare. Cataract, endoscopy, and colonoscopy procedures account for a substantial portion of national ASC case volume.

Palm Beach County already has multiple endoscopy, laser, eye-surgery, and general outpatient centers. A new GI or ophthalmology facility would need a clearly documented advantage, such as committed physicians with excess cases, a payer-network gap, a geographic access gap, lower patient cost, superior scheduling, or an existing practice seeking vertical integration. Without those conditions, these service lines are more likely candidates for acquisition or expansion than greenfield entry.

| Strategy | Relative risk | Best suited for |

|---|---|---|

| Existing-center expansion | Lower | Demonstrated capacity constraints |

| ASC acquisition | Moderate | Buyers seeking immediate market entry |

| Physician joint venture | Moderate | Groups with verified case volume |

| Hospital–physician joint venture | Moderate | Systems pursuing site-of-care migration |

| Specialty greenfield ASC | Moderate to high | Strong physician commitments and payer economics |

| General multispecialty greenfield ASC | High | Deep demand with limited competitive capacity |

| Indicator | Assessment | Interpretation |

|---|---|---|

| Demographic demand | Strong | Large and aging population |

| Outpatient revenue trend | Strong | Outpatient growth exceeds inpatient growth |

| Countywide ASC supply | High | Mature and competitive market |

| Hospital financial health | Mixed | Strong systems coexist with stressed providers |

| Reimbursement outlook | Moderately positive | 2026 update and procedure-list expansion |

| Greenfield multispecialty opportunity | Cautious | Requires anchor surgeons and verified leakage |

| Existing-center expansion | Attractive | Lower execution and ramp-up risk |

| Orthopedic and cardiovascular potential | Positive but conditional | Strong trends, meaningful existing competition |

| Western and north-county access | Potential gap | Must be validated through patient-origin data |

No reliable data in the source dataset establishes facility-level ASC profitability, case volume, operating-room utilization, payer mix, contracted reimbursement, specialty mix, or market share. This is not just a limitation of the dataset: CMS does not currently require ASCs to submit cost reports comparable to hospital cost reports, which is why MedPAC continues to recommend ASC cost-data reporting.

Before a lender or investor relies on a new-facility thesis, the analysis should obtain:

A market with strong outpatient demand can still be unsuitable for a particular project, location, specialty, or capital structure. A Wert-Berater ambulatory surgery center feasibility study converts the preliminary market indicators into a lender- and investor-usable decision framework.

For an owner or physician group, the study determines whether the opportunity should be pursued as a new center, expansion, acquisition, hospital partnership, or no-build strategy. For a lender, it establishes whether projected cash flow can support the proposed capital structure under both base and downside conditions. For a hospital or health system, it evaluates whether an ASC will create incremental value or merely move profitable cases out of an existing outpatient department. For investors, developers, and municipalities, it tests demand, competitive capacity, and absorption before capital is committed.

A complete analysis would typically include primary and secondary service-area definition, drive-time and patient-origin analysis, current and planned competitor inventory, specialty-level supply and demand, physician roster and procedure-volume validation, procedure eligibility and site-of-service migration, payer and reimbursement analysis, market-share and case-capture assumptions, facility size and operating-room requirements, the development and equipment budget, a staffing and anesthesia model, a ten-year operating pro forma, working-capital and ramp-up analysis, break-even case volume, debt-service coverage and lender ratios, base, downside, and severe-downside cases, and an independent feasibility conclusion. Our broader healthcare feasibility studies and hospital feasibility studies apply the same lender-grade discipline across facility types.

The Palm Beach County ASC market is supported by favorable demographics, strong outpatient growth, and continuing national migration of procedures into lower-cost ambulatory settings. It is also a mature market with significant existing capacity and concentrated competition.

The evidence favors targeted expansion, physician-aligned joint ventures, orthopedics and selected spine procedures, conditional cardiovascular development, and carefully located north- or west-county projects. It does not support a general conclusion that Palm Beach County needs another undifferentiated multispecialty surgery center.

Wert-Berater prepares independent ambulatory surgery center feasibility studies for physician owners, healthcare systems, developers, investors, and lenders. The analysis can evaluate market demand and competitive capacity, physician and procedure volume, payer mix and reimbursement, geographic service gaps, facility size and operating-room requirements, development and equipment costs, staffing and anesthesia assumptions, break-even case volume, debt-service capacity, and base and downside financial scenarios.

Contact Wert-Berater to evaluate a proposed Palm Beach County ambulatory surgery center, expansion, acquisition, or hospital–physician joint venture — or schedule a qualification Zoom to discuss scope.

Palm Beach County does not appear broadly underserved at the countywide level. The July 2026 dataset identifies 41 facilities, including 39 with CMS certification numbers. However, geographic and specialty gaps may still exist in north-county and western submarkets and in selected orthopedic, spine, cardiovascular, and physician-aligned services.

Orthopedics, total joints, selected spine procedures, and cardiovascular services appear to have favorable industry momentum. Any project would still require validation of surgeon commitments, procedure eligibility, payer reimbursement, existing competitive capacity, and patient demand.

Expansion can carry less risk when an existing facility has documented operating-room constraints, established payer contracts, experienced staff, and committed physician volume. Expansion is not automatically feasible; utilization by room, hour, specialty, and surgeon must first be verified.

Lenders should evaluate surgeon-specific procedure volume, payer mix, reimbursement by CPT code, operating-room utilization, patient origin, staffing, anesthesia coverage, development costs, equipment costs, working capital, break-even case volume, debt-service coverage, and downside scenarios.

A feasibility study tests whether the proposed market, location, specialty mix, surgeon base, facility size, reimbursement assumptions, and capital structure can support a sustainable operation. It can also compare greenfield development with expansion, acquisition, or joint-venture alternatives.

No. Case migration depends on clinical suitability, payer authorization, physician participation, procedure eligibility, patient characteristics, reimbursement, ownership relationships, and the hospital’s broader financial strategy.

Disclaimer: This article is provided for general informational and marketing purposes. It does not constitute legal, accounting, financial, investment, or lending advice, and it is not a feasibility study or an appraisal. Local financial calculations and facility counts are based on the Ambulatory Surgery Center Profiler dated July 14, 2026; hospital reporting periods vary from 2024 through 2025 and figures are drawn from each provider’s latest available public reporting. Market conditions, reimbursement policy, and regulatory requirements change. Readers should confirm current requirements with their lender, counsel, and professional advisers before making development or investment decisions.

President, Wert-Berater, Inc. — independent feasibility study consultants since 1998. More than 4,000 feasibility studies completed across all 50 states and internationally, evaluating $40.2 billion in project value for SBA, USDA, EB-5, conventional, and institutional financing decisions — including healthcare, medical facility, and lender-reviewed engagements. Fiduciary duty runs to the lender and agency in every engagement.

+1 310-857-2443 ext. 800 · email · 1968 South Coast Hwy, Ste 2382, Laguna Beach, CA 92651 · 111 Town Square Pl Ste 1238 PMB 657834, Jersey City, NJ 07310 · 539 W. Commerce St #8486, Dallas, TX 75208 · 66 W Flagler Street, Suite 900, PMB 12704, Miami, FL 33130

Schedule a ConversationSpeak with Wert-Berater about a proposed Palm Beach County ambulatory surgery center, expansion, acquisition, or hospital–physician joint venture. Provide the project location, proposed specialties, surgeon commitments, and lender requirements to receive a project-specific scope. Independent feasibility studies since 1998: 4,000+ engagements, $40.2 billion in evaluated project value.