Twenty-one of Los Angeles County’s largest hospitals — including Cedars-Sinai, Ronald Reagan UCLA, Keck Hospital of USC, and five Kaiser Permanente medical centers — hold Medicare Rural Referral Center status, a payment classification Congress created for large rural hospitals. Together they operate roughly 7,800 Medicare-certified beds and reported $20.0 billion in net patient revenue in their latest cost reports. This analysis explains how urban hospitals become “rural,” what the designation is commonly worth, how the 21 hospitals actually perform financially, and what the trend means for hospital developers, operators, and lenders.

Evaluating a rural or critical access hospital project? See our rural hospital and critical access hospital feasibility studies — independent, lender-grade analysis covering designation pathways, reimbursement, and debt capacity.

Want this analysis for your own market? Order a custom hospital or healthcare facility market report for any county or state — from $1,950, delivered in 3–5 business days.

Los Angeles County is the most populous county in the United States, with roughly 9.7 million residents in a metropolitan area of about 13 million. It contains no meaningful rural geography by any everyday definition. Yet a July 2026 hospital dataset identifies 21 Los Angeles County short-term acute care hospitals holding Medicare Rural Referral Center (RRC) status — a payment classification Congress created in the early 1980s for large rural hospitals that receive complex referrals from surrounding rural regions.

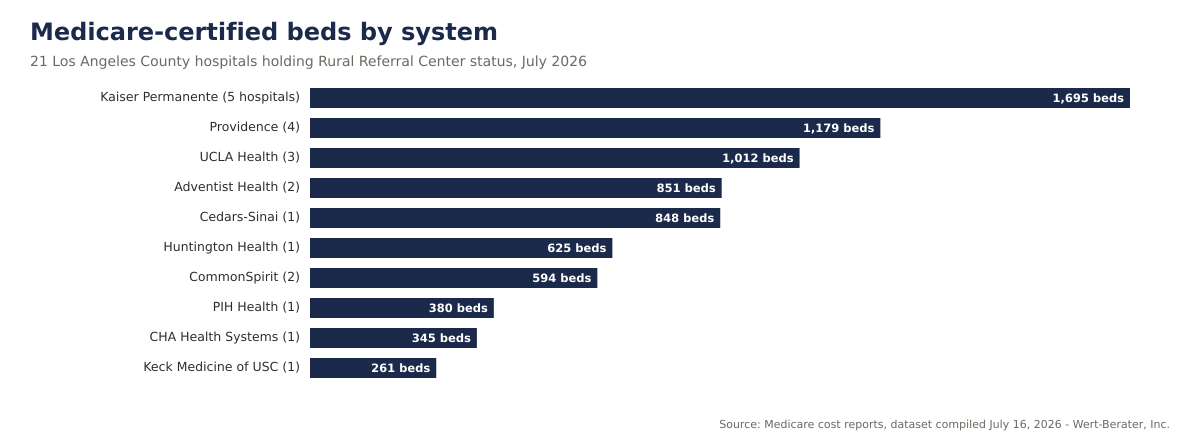

The roster is not a collection of obscure community hospitals. It includes Cedars-Sinai Medical Center, Ronald Reagan UCLA Medical Center, Keck Hospital of USC, Huntington Health in Pasadena, five Kaiser Permanente medical centers, four Providence hospitals, two Adventist Health hospitals, and two CommonSpirit hospitals. Together the 21 facilities operate roughly 7,790 Medicare-certified beds, employ about 59,300 people, and reported 348,615 discharges and 1.85 million inpatient days in their latest Medicare cost-report periods.

Key finding: Rural Referral Center status in Los Angeles County is a paper classification, not a geographic description — 18 of the 21 hospitals carry a CMS urban/rural designation of “Rural” despite operating in America’s largest urban county. The designation travels with meaningful Medicare payment and 340B drug-pricing advantages, and its spread to major urban systems is a payment-strategy trend that hospital developers, operators, and lenders should understand and model explicitly.

| Indicator | Market result |

|---|---|

| Los Angeles County hospitals with Rural Referral Center status | 21 |

| Facility type | All short-term acute care |

| Combined Medicare-certified beds | 7,790 |

| Combined discharges (latest cost-report periods) | 348,615 |

| Combined inpatient days | 1,846,281 |

| Combined gross patient revenue | $95.2 billion |

| Combined net patient revenue (latest periods) | $20.0 billion |

| Combined net income (latest periods) | $1.53 billion |

| Hospitals with positive net income | 11 of 21 |

| Hospitals participating in 340B drug pricing | 13 of 21 |

| CMS urban/rural designation shown as “Rural” | 18 of 21 |

Because Medicare law allows it. Under a provision Congress added in 1999 — codified at Section 1886(d)(8)(E) of the Social Security Act and implemented at 42 CFR §412.103 — a hospital located in a metropolitan area may apply to be treated as rural for Medicare inpatient payment purposes if it meets criteria set out in regulation. The hospital does not move; its paperwork does.

Once a hospital is treated as rural, a second regulation — 42 CFR §412.96 — opens the door to Rural Referral Center status. In general terms, a hospital qualifies as an RRC if it is rural for payment purposes and is large (the commonly cited threshold is 275 or more beds) or demonstrates referral-hospital characteristics such as high discharge volume and case-mix intensity. A 300-to-800-bed urban medical center satisfies the size test easily — the only hard step was becoming “rural” in the first place.

The result is visible throughout the dataset: every one of the 21 hospitals is flagged as a Rural Referral Center, 18 of the 21 carry a CMS urban/rural designation of “Rural,” and none holds the other classic rural designations — not one is a Sole Community Hospital, a Medicare Dependent Hospital, or a low-volume hospital. That pattern is the signature of the urban-to-rural reclassification strategy rather than of genuinely isolated rural providers. Industry and policy analyses have documented the same trend nationally: the number of RRCs has multiplied over the past decade, and a large share of them now sit in metropolitan areas.

Hospitals do not pursue paper reclassification for sentiment. RRC status interacts with several Medicare and federal drug-pricing provisions. The advantages most commonly cited by hospital advisers include:

Five health systems account for 16 of the 21 hospitals. Kaiser Permanente holds five designations, Providence four, UCLA Health three, and Adventist Health and CommonSpirit two each — alongside five prominent independents and single-system flagships.

| Hospital | City | System | Certified beds | Discharges | Inpatient days | 340B |

|---|---|---|---|---|---|---|

| Cedars-Sinai Medical Center | Los Angeles | Cedars-Sinai | 848 | 51,618 | 302,122 | Yes |

| Huntington Health | Pasadena | Independent (Cedars-Sinai affiliation) | 625 | 23,759 | 120,253 | Yes |

| Adventist Health Glendale | Glendale | Adventist Health | 515 | 16,907 | 82,449 | Yes |

| Kaiser Los Angeles Medical Center | Los Angeles | Kaiser Permanente | 507 | 22,329 | 127,070 | No |

| Ronald Reagan UCLA Medical Center | Los Angeles | UCLA Health | 445 | 22,799 | 181,776 | Yes |

| PIH Health Good Samaritan Hospital | Los Angeles | PIH Health | 380 | 10,418 | 45,213 | Yes |

| Providence Saint Joseph Medical Center | Burbank | Providence | 360 | 15,900 | 74,372 | Yes |

| Kaiser Downey Medical Center | Downey | Kaiser Permanente | 352 | 19,017 | 91,521 | No |

| CHA Hollywood Presbyterian Medical Center | Los Angeles | CHA Health Systems | 345 | 12,444 | 62,518 | No |

| Adventist Health White Memorial | Los Angeles | Adventist Health | 336 | 22,631 | 98,655 | Yes |

| UCLA Santa Monica Medical Center | Santa Monica | UCLA Health | 331 | 13,792 | 85,291 | Yes |

| Kaiser Panorama City Medical Center | Panorama City | Kaiser Permanente | 325 | 11,991 | 45,579 | No |

| Providence Saint John’s Health Center | Santa Monica | Providence | 317 | 11,719 | 53,277 | No |

| Glendale Memorial Hospital | Glendale | CommonSpirit | 304 | 8,686 | 36,440 | Yes |

| Kaiser West Los Angeles Medical Center | Los Angeles | Kaiser Permanente | 293 | 10,429 | 43,938 | No |

| California Hospital Medical Center | Los Angeles | CommonSpirit | 290 | 14,346 | 78,114 | Yes |

| The Keck Hospital of USC | Los Angeles | Keck Medicine of USC | 261 | 12,230 | 85,059 | Yes |

| Providence Holy Cross Medical Center | Mission Hills | Providence | 257 | 15,767 | 80,883 | Yes |

| Providence Cedars-Sinai Tarzana Medical Center | Tarzana | Providence | 245 | 13,595 | 59,655 | Yes |

| UCLA West Valley Medical Center | West Hills | UCLA Health | 236 | 8,096 | 48,509 | Yes |

| Kaiser Woodland Hills Medical Center | Woodland Hills | Kaiser Permanente | 218 | 10,142 | 43,587 | No |

| Combined | — | — | 7,790 | 348,615 | 1,846,281 | 13 of 21 |

Combined inpatient days against certified beds imply occupancy of roughly 65% across the roster, though the figure should be read loosely — certified-bed counts and cost-report day counts are not perfectly aligned at every facility, and individual hospitals range from the low 30s to effectively full. Aggregate average length of stay is about 5.3 days, typical for short-term acute care.

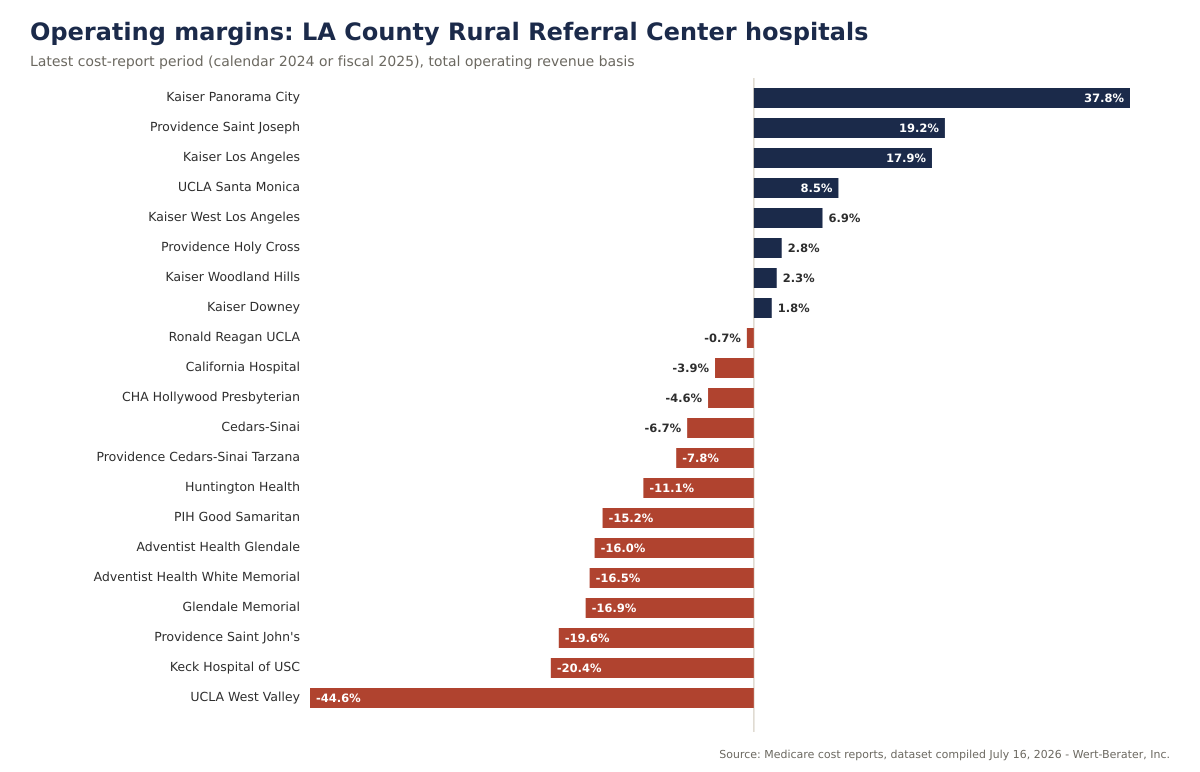

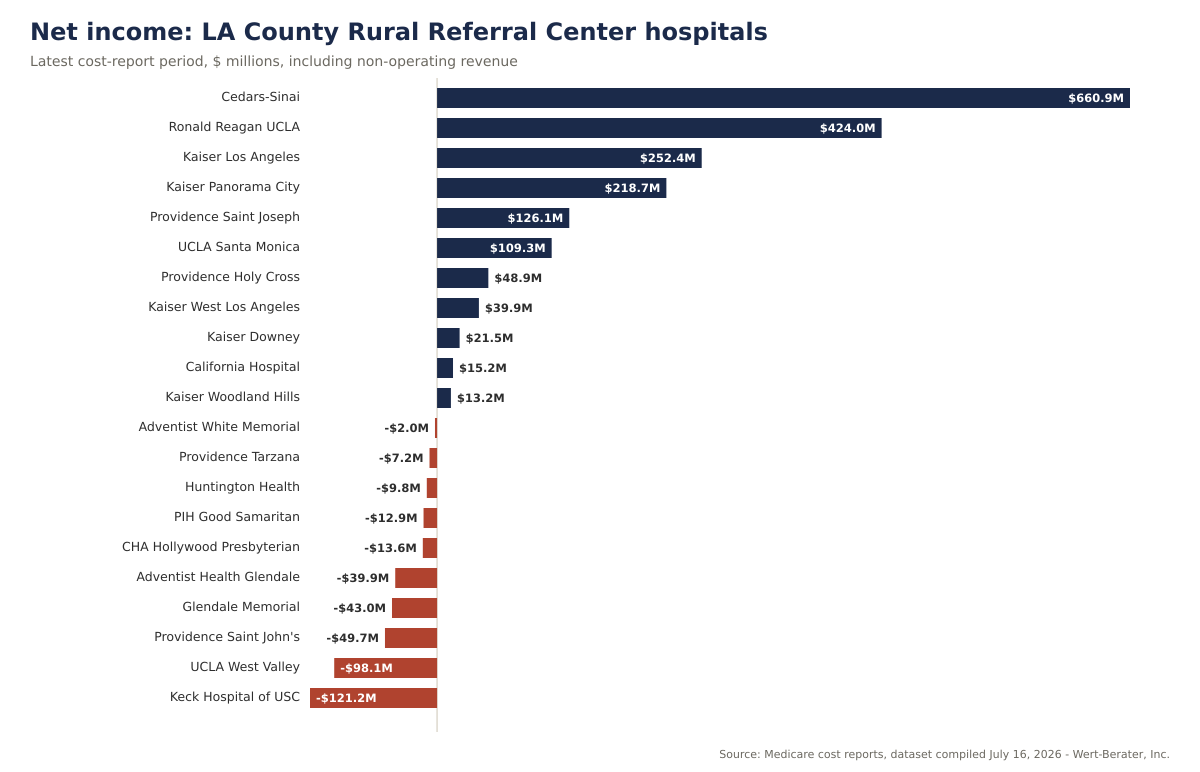

The 21 hospitals reported combined net patient revenue of $20.0 billion and combined net income of $1.53 billion in their latest cost-report periods — but the aggregate conceals extreme dispersion. Eight of 21 posted positive operating margins; 11 of 21 posted positive net income once non-operating revenue is included.

| Hospital | Period end | Net patient revenue | Operating margin | Net income |

|---|---|---|---|---|

| Cedars-Sinai Medical Center | 6/30/2025 | $4,400.6M | –6.7% | $660.9M |

| Ronald Reagan UCLA Medical Center | 6/30/2025 | $3,127.6M | –0.7% | $424.0M |

| The Keck Hospital of USC | 9/30/2025 | $1,476.1M | –20.4% | –$121.2M |

| Kaiser Los Angeles Medical Center | 12/31/2024 | $1,400.5M | 17.9% | $252.4M |

| Kaiser Downey Medical Center | 12/31/2024 | $1,028.7M | 1.8% | $21.5M |

| UCLA Santa Monica Medical Center | 6/30/2025 | $969.8M | 8.5% | $109.3M |

| Huntington Health | 6/30/2025 | $786.5M | –11.1% | –$9.8M |

| Providence Holy Cross Medical Center | 12/31/2024 | $631.8M | 2.8% | $48.9M |

| California Hospital Medical Center | 12/31/2024 | $610.7M | –3.9% | $15.2M |

| Adventist Health White Memorial | 12/31/2024 | $594.3M | –16.5% | –$2.0M |

| Providence Saint Joseph Medical Center | 12/31/2024 | $577.3M | 19.2% | $126.1M |

| Kaiser Panorama City Medical Center | 12/31/2024 | $575.9M | 37.8% | $218.7M |

| Kaiser West Los Angeles Medical Center | 12/31/2024 | $563.5M | 6.9% | $39.9M |

| Adventist Health Glendale | 12/31/2024 | $560.4M | –16.0% | –$39.9M |

| Kaiser Woodland Hills Medical Center | 12/31/2024 | $524.9M | 2.3% | $13.2M |

| CHA Hollywood Presbyterian Medical Center | 12/31/2024 | $500.5M | –4.6% | –$13.6M |

| Providence Saint John’s Health Center | 12/31/2024 | $464.1M | –19.6% | –$49.7M |

| PIH Health Good Samaritan Hospital | 9/30/2025 | $390.5M | –15.2% | –$12.9M |

| Providence Cedars-Sinai Tarzana Medical Center | 12/31/2024 | $344.9M | –7.8% | –$7.2M |

| Glendale Memorial Hospital | 12/31/2024 | $288.4M | –16.9% | –$43.0M |

| UCLA West Valley Medical Center | 6/30/2025 | $223.0M | –44.6% | –$98.1M |

| Combined | — | $20,040.0M | — | $1,532.6M |

Three distinct financial stories sit inside one designation:

All five Kaiser hospitals posted positive operating margins — Panorama City’s 37.8% and Los Angeles Medical Center’s 17.9% are the two strongest results in the county roster. Kaiser’s integrated payer-provider model makes its cost reports unusual: “revenue” largely reflects internal transfer pricing from Kaiser’s health plan, and the hospitals report essentially zero days cash on hand because treasury is managed at the system level, not the facility. The margins are real signals of system allocation, not standalone-hospital economics — and none of the five participates in 340B, consistent with a closed integrated pharmacy model.

Cedars-Sinai (–6.7% operating margin, $660.9 million net income), Ronald Reagan UCLA (–0.7%, $424.0 million), and California Hospital (–3.9%, $15.2 million) all lost money on operations yet finished profitable on investment income, philanthropy, and system support. Keck Hospital of USC is the outlier: a –20.4% operating margin and a $121.2 million net loss in its latest period despite $1.48 billion of net patient revenue. UCLA West Valley — a recently acquired turnaround campus — posted the roster’s deepest loss at –44.6% operating margin and –$98.1 million net income, with negative days cash on hand.

Glendale Memorial (–16.9% operating margin, negative 19.5 days cash on hand), Adventist Health Glendale (–16.0%, five consecutive years of operating losses, 1.3 days cash), Adventist Health White Memorial (–16.5%), PIH Good Samaritan (–15.2%), and Providence Saint John’s (–19.6%) show the classic profile of urban safety-net and community hospitals under payer-mix and labor-cost pressure. For this group, designation-linked revenue — uncapped DSH, 340B savings — is not a strategic bonus; it is operating oxygen.

If the largest hospitals in urban California find it worthwhile to hold a rural payment classification, smaller operators and developers should treat Medicare designation analysis as a first-order feasibility input, not an afterthought. The reimbursement difference between a correctly and incorrectly classified facility can move a project’s debt-service coverage materially in either direction.

A developer of an actual rural hospital — a critical access hospital, a Sole Community Hospital, or a rural emergency hospital — now competes for programs and payment pools alongside sophisticated urban systems that hold rural classifications. Policy analysts have noted that the growth of urban RRCs has, at times, affected rural wage-index calculations and 340B program composition. A rural project’s feasibility study should anticipate that designation-linked benefits are shared with — and shaped by — urban participants.

Thirteen of the 21 hospitals participate in 340B. For hospitals with substantial outpatient and specialty drug volume, 340B margins can rival core patient-care margins — and eligibility pathways (including the lower RRC threshold) are precisely what the reclassification strategy protects. Any acquisition or expansion involving a 340B hospital should model the sensitivity of cash flow to 340B contraction scenarios, which remain a live policy debate.

A strategy built on paper classifications is exposed to the pen that wrote them. The urban-to-rural pathway has been the subject of repeated federal rulemaking attention, litigation, and budget-scoring interest. Lenders financing hospitals whose margins depend on designation-linked revenue should quantify the downside case in which the benefit narrows — exactly as they would stress-test an interest-rate or census assumption.

Ten of the 21 hospitals posted negative net income, and several combine deep operating losses with thin or negative liquidity. That profile historically precedes ownership changes, service-line restructurings, and system consolidations — each of which triggers the need for independent market and financial feasibility analysis, whether for a buyer, a lender, a bondholder, or a state regulator.

| Indicator | Assessment | Interpretation |

|---|---|---|

| Scale of the RRC roster | Exceptional | 21 hospitals, 7,790 certified beds, $20.0B net patient revenue |

| Geographic character | Urban | Designation is regulatory, not geographic; 18 of 21 flagged “Rural” by classification |

| System concentration | High | Five systems hold 16 of 21 designations |

| Operating profitability | Weak overall | 8 of 21 positive operating margins; median hospital loses money on operations |

| Bottom-line profitability | Mixed | 11 of 21 positive net income; $1.53B combined, concentrated in a few winners |

| 340B participation | Majority | 13 of 21 hospitals; lower RRC threshold is a common eligibility pathway |

| Financial dispersion | Extreme | Operating margins span +37.8% to –44.6% |

| Policy risk | Material | Designation-linked benefits subject to rulemaking and legislative change |

The dataset establishes classifications, utilization, and cost-report financial performance, but several decisive facts are not visible in public reporting. Before relying on a designation-driven thesis — for an acquisition, an expansion, a bond issue, or a competing project — the analysis should obtain:

Designation-driven reimbursement is exactly the kind of input that separates a lender-grade feasibility study from a marketing document. A Wert-Berater rural hospital and critical access hospital feasibility study models the project’s realistic designation pathway — critical access, Sole Community, Medicare Dependent, Rural Referral Center, or rural emergency hospital — and quantifies what each is worth under current rules and under downside scenarios where the rules tighten.

For an operator or developer, the study determines whether a proposed hospital, conversion, or expansion is feasible under the reimbursement it can actually obtain — not the reimbursement a best case assumes. For a lender, it establishes whether projected cash flow covers the proposed capital structure when designation-linked revenue is stressed. For a health system, it evaluates acquisition and affiliation candidates — including distressed urban hospitals like several in this dataset — on defensible market and financial evidence. Our broader healthcare feasibility studies and hospital feasibility studies apply the same lender-grade discipline across facility types.

And if you are evaluating a different geography, Wert-Berater prepares this same analysis for any county or state in the United States: custom hospital and healthcare facility market reports start at $1,950 and are delivered in 3–5 business days.

Los Angeles County’s 21 Rural Referral Centers are a case study in how Medicare payment policy actually works: classifications created for one purpose become strategic assets for another, and the institutions best equipped to capture them are the largest and most sophisticated. The designation now sits on hospitals reporting $95.2 billion in gross charges in America’s densest urban market.

The financial data show why the strategy matters — and why it is not a cure. Designation-linked revenue has not rescued Glendale Memorial, Keck, or the county’s other operating-loss hospitals from structural payer-mix and cost pressure, while the strongest performers would likely be strong under any classification. For developers, operators, and lenders, the lesson is discipline: model designations explicitly, value their benefits conservatively, and never let a paper classification substitute for demand, payer, and cost fundamentals.

Wert-Berater prepares independent hospital feasibility studies for operators, health systems, developers, investors, and lenders — including rural hospital, critical access hospital, and rural emergency hospital engagements where Medicare designation strategy is decisive. The analysis can evaluate market demand and competitive capacity, payer mix and designation-linked reimbursement, program requirements, development costs, staffing assumptions, break-even utilization, debt-service capacity, and base and downside financial scenarios.

Contact Wert-Berater to evaluate a proposed hospital project, conversion, acquisition, or expansion — or schedule a qualification Zoom to discuss scope.

A Rural Referral Center is a Medicare payment classification Congress created in the early 1980s for large rural hospitals that operate like urban referral hospitals — treating complex cases referred from a wide region. Qualification generally requires the hospital to be treated as rural for Medicare payment purposes and to meet size or referral-pattern criteria, such as a large bed count or high discharge volume and case-mix intensity. The designation changes how several Medicare payment provisions apply to the hospital.

Federal law allows a hospital located in a metropolitan area to elect treatment as rural for Medicare payment purposes if it meets criteria set out in regulation. Once reclassified as rural, a large urban hospital typically satisfies the Rural Referral Center size criteria easily. In the July 2026 dataset, 18 of the 21 Los Angeles County hospitals carry a CMS urban/rural designation of Rural despite operating in one of the nation’s densest urban markets — the paper classification, not the geography, drives the payment treatment.

Commonly cited advantages include exemption from the payment cap that otherwise limits rural hospitals’ Medicare disproportionate share payments, eligibility for the 340B drug pricing program at a lower disproportionate-share threshold than other hospitals, and relief from proximity requirements when seeking reclassification to a higher wage index. The value varies by hospital: it depends on payer mix, drug spend, and wage-index geography, and the underlying rules are subject to change.

Designation-driven economics cut both ways. A project pro forma that ignores available designations can understate achievable reimbursement, while one that depends on a designation surviving future rulemaking carries policy risk that lenders should price. Any hospital feasibility study — urban or rural — should model reimbursement under the facility’s realistic designation pathway and stress-test the downside where a designation-linked benefit is reduced or eliminated.

Disclaimer: This article is provided for general informational and marketing purposes. It does not constitute legal, accounting, financial, investment, or lending advice, and it is not a feasibility study or an appraisal. Hospital financial figures are drawn from Medicare cost reports and utilization data compiled July 16, 2026; reporting periods vary from calendar 2024 through fiscal years ending September 2025, and cost-report entities may include operations beyond a single hospital. Gross patient revenue reflects charges before contractual allowances and is not comparable to net revenue. Medicare classification rules, reimbursement policy, and the 340B program are described in general terms only and change through rulemaking and legislation; classification flags reflect the dataset date and should be verified against current CMS records. Readers should confirm current requirements with their lender, counsel, and professional advisers before making development or investment decisions.

President, Wert-Berater, Inc. — independent feasibility study consultants since 1998. More than 4,000 feasibility studies completed across all 50 states and internationally, evaluating $40.2 billion in project value for SBA, USDA, EB-5, conventional, and institutional financing decisions — including healthcare, medical facility, and lender-reviewed engagements. Fiduciary duty runs to the lender and agency in every engagement.

+1 310-857-2443 ext. 800 · email · 1968 South Coast Hwy, Ste 2382, Laguna Beach, CA 92651 · 111 Town Square Pl Ste 1238 PMB 657834, Jersey City, NJ 07310 · 539 W. Commerce St #8486, Dallas, TX 75208 · 66 W Flagler Street, Suite 900, PMB 12704, Miami, FL 33130

Schedule a ConversationSpeak with Wert-Berater about a proposed hospital project, rural or critical access hospital, conversion, acquisition, or expansion. Provide the project location, proposed bed count and programs, designation strategy, and lender requirements to receive a project-specific scope. Independent feasibility studies since 1998: 4,000+ engagements, $40.2 billion in evaluated project value.