Assisted Living Facility Feasibility Study Consultants, Wert-Berater, Inc. Executive Snapshot: 2025 Demand & Supply Signals Occupancy & Supply: Senior housing occupancy in the 31 NIC MAP primary markets…

Assisted Living Facility Feasibility Study Consultants, Wert-Berater, Inc. Executive Snapshot: 2025 Demand & Supply Signals Occupancy & Supply: Senior housing occupancy in the 31 NIC MAP primary markets climbed to 88.1% in Q2 2025 , while annual inventory growth fell below 1% (0.97%) , the lowest since tracking began—clear evidence of tight supply and strong absorption. National Investment Center

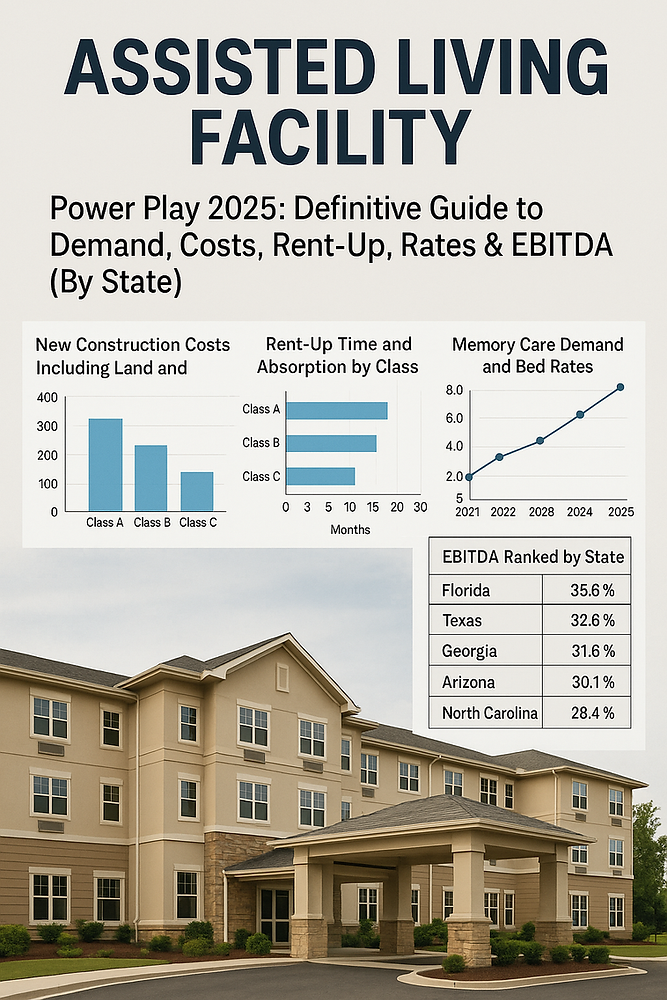

Costs & Pricing: The national median assisted living monthly rate reached $5,900 in 2024 , up ~10% YoY , according to Genworth/CareScout’s Cost of Care Survey. Memory care medians nationally commonly sit higher; recent trackers show national memory care medians in the $6,100–$7,300/month range. Carescout

Construction: Benchmark studies show seniors housing hard costs in the mid-$300s to high-$300s per square foot depending on level and finish, with assisted living “mid-level” commonly $374–$349/sf in 2024; site/land and soft costs push total development costs above $300k per unit on average. Senior Housing News

Why the squeeze? Baby-boomer aging (80+ cohort) is accelerating while new starts remain muted. NIC notes record-low construction starts through 2024–2025; multiple sources expect demand to outstrip new supply for the next several years. National Investment Center, MarketWatch

Rule of thumb (2025): Total development budget per assisted living unit (Class B/A-): $325k–$450k in most Sun Belt/Heartland metros; $450k–$650k (or higher) in constrained coastal markets, inclusive of land, softs, and FF&E—assuming 350–450 net rentable sf/unit and modern common spaces. (Synthesis of CBRE, trade coverage, and current contractor briefs.) CBRE, Senior Housing News

Permitting and regulatory friction can materially inflate carrying costs. Example: Hawaii research shows outsized regulatory cost burden in residential development—a cautionary signal for any island/coastal entitlement path. AP News

Care Revenue Model (Illustrative):

Underwriting guardrails (stabilized, private-pay AL):EBITDA margin: 24–32% ; Management fee: 5–6% EGI; Capex reserve: $300–$400/unit-yr (Class A) rising with building complexity. (Synthesis of ASHA benchmarks + market commentary.) Senior Housing News

Demand strength blends share of 65+ and 80+ cohorts , migration inflows , household wealth , and limited new supply . Current indicators:

“Demand Score” (illustrative, combining 65+ share, migration trend, and low inventory growth):

Rank

State

Example High-Demand Metros

Why It Scores

Florida

Tampa, Orlando, Naples

High 65+ share, strong in-migration, constrained new starts

Arizona

Phoenix, Tucson

Rapid senior growth, Sun Belt migration

Texas

DFW, Austin, San Antonio

Nation-leading population growth; select senior hubs growing fast

South Carolina

Myrtle Beach, Greenville

Fastest-growing senior metro; coastal draw

North Carolina

Raleigh-Durham, Charlotte

In-migration + high HH incomes

Tennessee

Nashville, Knoxville

65+ rising to ~20% by 2040; business-friendly

Georgia

Atlanta suburbs, Savannah

Migration + relative affordability

Nevada

Las Vegas, Reno

Retiree in-migration, tax climate

Maine

Portland, Bangor

Very high 65+ share; limited supply

10

Colorado

Denver exurbs, Colorado Springs

Affluent households; limited infill supply

(Sources reflect recent occupancy/supply signals, demographic shares, and migration coverage.) Houston Chronicle, National Investment Center, World Population Review

Region

Typical Range (AL, stabilized plan)

Notes

Coastal urban/infill (CA, MA, WA, HI)

$80k–$250k+ / bed

Tight sites, lengthy entitlements; financing carry adds risk. CBRE+1

High-growth Sun Belt suburbs (FL, TX, AZ, NC, SC, TN, GA)

$35k–$60k / bed

Abundant entitled suburban parcels; premiums for corner visibility. CBRE

Heartland & tertiary

$20k–$30k / bed

Lower land costs but smaller qualified demand radius. CBRE

These ranges derive from site-acquisition shares in CBRE’s development study combined with current AL hard/soft cost contexts and typical GBA/unit assumptions. Always verify with recent broker land comps and municipal fees. CBRE

Variable

Base Case

Low Case

High Case

Impact

Total Dev Cost/Unit

$400,000

$350,000

$475,000

Affects return on cost; leverage limits

Average AL Rent

$5,900

$5,400

$6,400

RevPAR & margin swing driver Carescout

Lease-Up to 90%

24 months

30 months

18 months

Carry, TI/marketing burn

Care Fees/Unit (avg)

$2,200

$900

$2,500

ADL intensity & staffing mix

OpEx/Unit/Month

$3,500

$3,800

$3,200

Wages, insurance, utilities

Stabilized EBITDA Margin

28%

24%

32%

Value & DSCR tolerance Senior Housing News

Exit Cap (AL/MC)

6.75%

7.25%

6.25%

Sensitivity to rate regime

Q1. What’s the current national occupancy and why is it rising?A. NIC reports 88.1% occupancy in Q2 2025 across primary markets, with inventory growth under 1% due to years of low new starts—demand is outpacing supply. National Investment Center

Q2. What does it cost to build an Assisted Living Facility today?A. Inclusive of land, softs, and FF&E, many projects pencil $325k–$450k per unit in Sun Belt/Heartland metros, $450k–$650k+ in coastal/infill. Hard costs often $374–$349+/sf for mid-level AL (2024). Senior Housing News

Q3. How long will lease-up take?A. Plan 18–30 months to stabilization. Strong pre-leasing and first-year momentum are critical; NIC shows first-year velocity heavily influences outcomes. Senior Housing News

Q4. What are typical Assisted Living Facility room rates?A. The national median AL rate was $5,900/month (2024) . Private rooms trend higher; semi-private lower. Memory care often ranges ~$6,100–$7,300+ nationally. Carescout

Q5. How do ADLs/IADLs affect revenue?A. ADLs (e.g., bathing, dressing) and IADLs (e.g., meds, shopping) define care tiers and fees. Clear documentation supports pricing and compliance. Centers for Medicare & Medicaid Services

Q6. What EBITDA margins are achievable?A. Stabilized AL/AL+MC commonly underwrite ~24–32% EBITDA margins , with IL-heavy mixes often higher. 2023 ASHA medians: IL ~32.5%, AL components ~29.2%, mixed campuses ~26.6%. Senior Housing News

Q7. Which states and cities show the greatest demand right now?A. Florida, Arizona, Texas, the Carolinas, Tennessee, Georgia lead on senior growth and in-migration; Myrtle Beach, SC is the fastest-growing senior metro, and Texas led absolute population growth in 2024. Pair this with low new starts to find the best submarkets. AP News, Houston Chronicle

Q8. What’s land per bed by state?A. There’s no one number: CBRE’s study places site acquisition ~8.2% of total development cost on average. Translating to per-bed often yields $20k–$30k in tertiary/Heartland markets, $35k–$60k in Sun Belt suburbs, and $80k–$250k+ for coastal urban infill. Validate with current local comps. CBRE

The Assisted Living Facility thesis in 2025 is straightforward: aging demand is accelerating while new supply remains historically constrained. That combination supports rents, absorption, and margins—but only for projects that buy the dirt right , control costs , design for care acuity , and win the first year of lease-up .

One external resource to track monthly: the NIC blog & NIC MAP Vision updates for occupancy, rate growth, and pipeline—crucial for timing new starts and underwriting rent growth. National Investment Center, National Investment Center

Sources referenced throughout:

Donald Safranek, President, Wert-Berater, Inc. Feasibility Study Consultants Feasibility Study Consultants

Wert-Berater, Inc.

1968 South Coast Highway

Suite 2382

Laguna Beach CA 92651

President, Wert-Berater, Inc. — independent feasibility study consultants since 1998. More than 4,000 feasibility studies completed across all 50 states and internationally, evaluating $40.2 billion in project value for SBA, USDA, EB-5, conventional, and institutional financing decisions. Fiduciary duty runs to the lender and agency in every engagement.

+1 310-857-2443 ext. 800 · email · 1968 South Coast Hwy, Ste 2382, Laguna Beach, CA 92651 · 111 Town Square Pl Ste 1238 PMB 657834, Jersey City, NJ 07310 · 539 W. Commerce St #8486, Dallas, TX 75208 · 66 W Flagler Street, Suite 900, PMB 12704, Miami, FL 33130

Schedule a ConversationIndependent feasibility studies since 1998 — 4,000+ engagements, $40.2 billion in evaluated project value. Standard delivery in 10 to 15 business days. Fiduciary duty to the lender and agency.